VA loans are a type of mortgage offered almost exclusively to veterans and military members as a thank-you for their service. They feature benefits that make it easier for veterans and their families to become homeowners, which can help build wealth and stability for their future.

If you plan on taking advantage of your VA loan benefit, you should know that a Certificate of Eligibility (COE) is required. But there’s no need to stress! We’ve got you covered with this guide.

Key Takeaways

- You need a VA Certificate of Eligibility to obtain a VA loan. There are 3 ways to get one: by mail, online, or through a lender.

- A VA Loan COE is different from a “COE” used for the G.I. Bill. You cannot use the same document for either.

- Your COE tracks your entitlement amount

Table of Contents

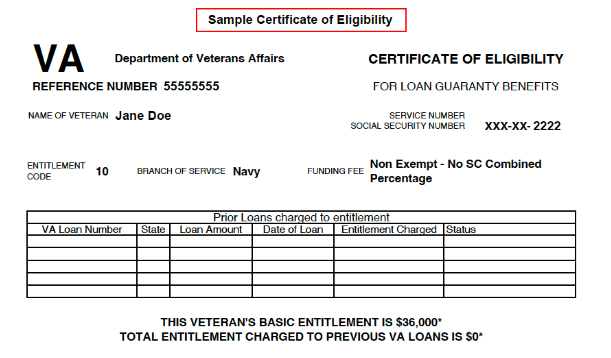

What is a VA Loan Certificate of Eligibility?

A Certificate of Eligibility is a core document that confirms your service requirements. You need it to secure a VA home loan. The COE shows lenders that you have served the required amount of time in the U.S. military to obtain a VA loan and keeps track of how many VA loans you’ve taken out. It also shows if you’re exempt from paying the VA funding fee.

Above, on the sample COE, you’ll see “non-exempt” next to the funding fee line. If you qualify for a funding fee exemption, you’ll see “exempt” on your form. If you haven’t used your VA benefit before, you’ll also see “No SC Combined Percentage” which indicates that you haven’t used the funding fee in the past (subsequent uses of the VA loan require a reduced funding fee payment).

You’ll also see the “Entitlement Code” line. Entitlement codes range from 01 to 11 and indicate to lenders either the period in which you served (for first-time applicants) or the status of your previous VA loans.

G.I. Bill COE vs. VA Loan COE

The GI Bill Certificate of Eligibility, which is actually referred to as a “Statement of Benefits” by the VA, serves different purposes from the VA Loan Certificate of Eligibility.

The GI Bill COE verifies a servicemember or veteran’s eligibility for education benefits under the Post-9/11 GI Bill and the Montgomery GI Bill and requires a completely separate document—the VA Form 22-1990– for application.

How to Get a VA Certificate of Eligibility

You can apply for a VA loan Certificate of Eligibility in three different ways:

- Apply online at the VA’s eBenefits Portal, which lists all the acceptable documents to upload as proof of your service. This is often the quickest method and will supply you with a downloadable PDF document right away.

- Apply through your VA-approved lender if you want to complete the full VA loan application in one place.

- Apply by mail by printing and mailing in VA Form 26-1880 from the Veteran’s Information Portal. You can expect to receive a copy of your COE by mail within 4-6 weeks.

If you apply for your Certificate of Eligibility through your lender or online through the eBenefits portal, you can receive it within a few minutes. If you use mail, the VA states processing times of 4 to 6 weeks.

Whichever method of application is chosen, all applicants are expected to provide personal identifying information such as name, date of birth and social security number. However, there is a bit of nuance to the additional information the VA needs to complete your unique Certificate of Eligibility. Let’s take a look.

VA Loan COE For Veterans

To get a COE, veterans need to provide proof of military service through forms such as DD-214 and other discharge paperwork.

The VA wants to ensure that you served for the minimum number of days required to qualify for a VA loan and were discharged under honorable conditions.

Some of the most important information that you’ll see on a DD-214 form include:

- Rank

- Place of entry

- Last duty assignment

- Records of service

- Primary duty specialty

- Remarks

- Character of service

VA Loan COE For National Guard and Reserve Members

Reservists and National Guard members need to provide their most recent annual retirement points summary along with proof of honorable service.

Army and Air National Guard members can submit either the NGB Form 22, which details separation and service records, or the NGB Form 23 points statement.

Reservists and National Guard members must present a signed statement of service. This document should include the required personal details and clearly confirm that the individual is an active Reservist or Guard member.

VA Loan COE For Surviving Spouses

Surviving spouses must provide proof of their relationship to the deceased veteran through a document such as a marriage certificate.

They must also offer evidence of the veteran’s military service through a form such as a DD-214 or other discharge paperwork.

VA Loan Statement of Service

If you’re an active duty servicemember you may need to submit a separate form known as a statement of service. This form includes information like:

- Name of your commanding officer

- Branch of service

- Unit of assignment

- Rank

- Active duty service date

- Expected discharge and discharge character

- Medals, badges and citations awarded

There’s no official form for a statement of service. Instead, a letter on official military letterhead is sufficient. Your specific loan officer can give you more guidance here, but you can typically get the job done by going to the head of your unit for a signature and official letterhead.

Check your VA Home Loan eligibility and get personalized rates. Answer a few questions and we'll connect you with a trusted VA lender to answer any questions you have about the VA loan program.

What if my COE gets denied?

If your Certificate of Eligibility gets denied, it may be because you didn’t provide sufficient evidence or you do not currently meet the eligibility requirements. Reach out to your local VA office for more guidance.

Does a COE expire?

A VA Certificate of Eligibility does not expire, but there are situations where you may need to get it updated.

Here are three common situations:

- You want to use the VA loan again: You typically use your VA home loan entitlement every time you use a VA loan. If you want to buy another home with a VA loan, you’ll need an updated COE to show the status of your entitlement—which may be reduced or fully restored depending on how you handled your first home sale. This process can be complicated for some lenders, so see our VA loan entitlement guide for more information.

- Your service status changes: If there is a change in your eligibility status (say you were active duty when you got your first loan, but you want another loan and you’re now separated) your COE will likely need to be updated.

- You’re working with a new lender: Some lenders might request a more recent COE to ensure all information is up-to-date, even though the original COE itself does not expire.

Generally, it’s always a good idea to check with the VA or a lender to confirm the status and validity of the COE before proceeding with a VA home loan application.

Does a COE guarantee my loan approval?

Getting your Certificate of Eligibility does not equal VA loan approval. It is only one step of the eligibility process for a VA loan. You must also meet employment and income requirements set by lenders.

The Bottom Line

While the specific requirements for obtaining a COE may vary depending on the individual’s circumstances and the type of benefit they are seeking, the VA has made the process relatively straightforward and accessible. Once you have your COE, you’re one step closer to accessing VA loan benefits, including lower interest rates, no down payment, and accessible credit score qualifications.

Equal Housing Opportunity. The Department of Veterans Affairs affirmatively administers the VA Home Loan Program by assuring that all Veterans are given an equal opportunity to buy homes with VA assistance. Federal law requires all VA Home Loan Program participants – builders, brokers and lenders offering housing for sale with VA financing – must comply with Fair Housing Laws and may not discriminate based on the race, color, religion, sex, handicap, familial status, or national origin of the Veteran.

About the comments on this site:

These responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.